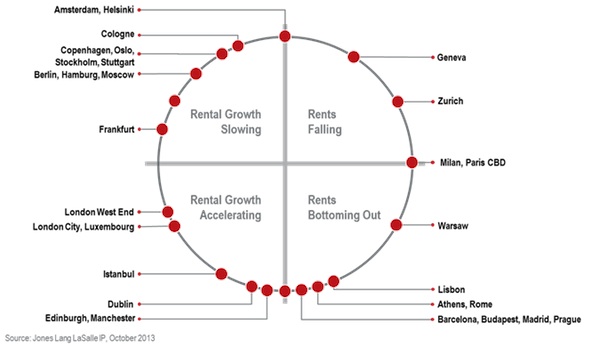

According to Jones Lang LaSalle’s Q3 European Office Property Clock, European office sector recovery continuing, but divergence in speed and strength remains. Strong on-going demand for quality space in key cities is propelling momentum. Over the quarter, the European Office Rental Index decreased by 1.1% as a result of rental declines recorded particularly in Paris (-7.2%), but also in Milan (-4.2%), Prague (-2.4%) and Barcelona (-1.4%). The contrasting prime rental increases in London (+2.6%), Munich (+1.6%) and Frankfurt (+1.5%), based on a combination of healthy demand and a shortage of quality stock, were not sufficient to offset these falls. Prime rents in all other Index markets remained stable.

The recovery of the European office sector continues, with the outlook improving alongside improvements in economic sentiment and growth. Conditions remain diverse, with markets moving at varying speeds. Occupiers do however remain vigilant and improving sentiment is likely to be vulnerable to external shocks. While the London office market is witnessing a rapid increase in momentum, the German and Nordic centres, while continuing to perform, are experiencing decreasing momentum. Conditions in Paris are impacted by on-going headwinds on the economic side. The Southern European centres as well as the CEE markets have reached, or are close to, the bottom of the cycle.

For the remainder of the year, rental growth is forecast to be limited on aggregate. However, London is expected to outperform, with on-going strong demand for quality space. The German centres as well as Oslo and Stockholm could see further growth, though momentum is slowing. Prime rents in Paris are expected to remain stable, and are not forecast to increase until mid-2014. At the same time, markets with still challenging economic conditions such as the Southern European centres, or markets with supply issues such as Warsaw, could see slight rental reductions.

(In the photo: Google Offices, London)